The value of a “Payments Reference Architecture” in driving payments transformation

With the Payments IT landscape frequently changing due to regulations, customer needs, and innovations, Financial Institutions (FIs) face challenges of high cost, slow pace of change, operational complexities, and a constant struggle to meet the goals of their payments business strategy. This creates a need to reassess their payments architecture and transform to enable agility and flexibility, and reduce costs.

To do so, FIs need a “Payments Reference Architecture” (PRA) which embodies industry best practices, enabling them to assess and define a target architecture meeting their payments business strategy and wider technology strategy. However, many FIs either do not have a well-defined PRA or have one which needs a refresh in line with current industry context and best practices.

This blog explores the need for a Payments Reference Architecture, the benefits it can provide, its features and how Icon’s own PRA helps Financial Institutions drive innovation and transformation.

Need for a Payments Reference Architecture and the benefits it provides to Financial Institutions

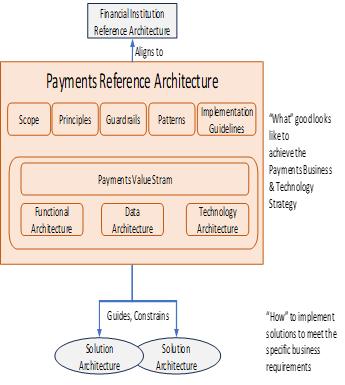

What is a Payments Reference Architecture (PRA)?

A PRA provides a view of “what good looks like” by laying the functional and technical foundation for the payments domain within the Financial Institution; it also guides and constrains the implementation of solutions as part of the various business and regulatory programmes of work undertaken.

Why do Financial Institutions need one?

Many FIs face challenges in their payments transformation journey related to the duplication of capabilities across the payments domain, the inconsistent integration with other domains within the FI, the increased resiliency risks as volumes of payments grow, and the high impact of industry changes e.g. SEPAInst, FedNow, and UK NPA. All of this leads to high costs, a reduced pace of change, high operational complexities, and hinders the ability to innovate in the current highly competitive landscape.

What are the benefits of a Payments Reference Architecture to Financial Institutions?

A PRA provides a common and authoritative view of the payments domain and its integration with other domains (e.g. Anti-Financial Crime, Core Banking, Customer, Data, and Channels), which guides and constrains instantiation of solution architectures, reduces cost by avoiding duplication of services, and defines a common vocabulary between Business and IT.

By decoupling the payments value chain, a PRA enables FIs to take decisions around “Buy” vs “Build”, by highlighting capabilities which are “commodity” versus “value add”. For example – Payment Execution/Clearing & Settlement functions are highly commoditised with limited potential for differentiation compared to Payment Initiation Management offering opportunities for innovation. This in turn increases agility and provides effective utilisation of resources.

A PRA also reduces operational costs through application rationalisation by identifying duplication of capabilities across applications and technical debt hotspots.

Finally, it provides the guidance to draw out the payments architecture roadmap as part of the FIs transformation journey.

Icon’s Payments Reference Architecture

Icon has developed its own PRA based on the extensive experience gained through various client engagements and practical experience gained from developing its own payments platform: IPF. The PRA is maintained through regular updates to accommodate client feedback and new industry developments around value-added services, to ensure the architecture is kept relevant and fit-for-purpose.

Icon’s Payments Reference Architecture provides –

Icon’s Payments Reference Architecture provides –

- Definition of the Payments Value Stream applying the design principle of decoupling the value chain

- Functional Architecture defining a set of services aligned to the business capability model with a clear demarcation of where these services should ideally sit within the Payments Value Stream

- Data Architecture describing the payments data lifecycle from capture, processing, storage, consumption, and a reference data model.

- Technology Architecture to realise the functional architecture aligned to the Financial Institution’s wider Technology Strategy

- Principles, Guardrails, Architecture Patterns and Implementation Guidelines based on industry best practices and practical experiences gained from implementing payment architectures.

Icon engages with FIs to assess and define their Payments Technology Strategy, enabling them to accelerate their payments transformation journey and generate greater business value from payments. As part of these engagements, Icon uses its PRA to:

- Assess the FI’s current payments architecture and identify hotspots – e.g., duplication of capabilities, technical debt, integration complexity.

- Define the target payments architecture, applying Icon’s best practice guardrails and architecture patterns, in conjunction with the FI’s own technology strategy and standards.

- Define an architecture roadmap to migrate to the target architecture, defining the business value realised and the application rationalising opportunities at each transition state.

Conclusion

FIs either starting or already on their payments transformation journey, need to re-assess and define their payments architecture using a PRA which defines “what good looks like”. The value of a well-defined PRA is that it enables agility, lowers cost and improves operational efficiency by providing a common view of the payments domain within the FI organisation. Moreover, it enables “Build” vs “Buy” decisions by decoupling the payments value chain, introduces application rationalisation opportunities and provides guidance to the transformation roadmap: driving true transformation in payments.

Speak to our expert team about how Icon can help Financial Institutions accelerate their payments transformation journey using its PRA. Case studies for some of Icon’s engagements are available here:

Ranga Natraj