The European Payments Initiative – Back to the Future

In July 2020, a group of sixteen major European banks from five Euro countries announced the launch of the European Payments Initiative (EPI) with the aim of creating a unified payment solution for consumers and merchants across Europe.

‘A grandiose task’, we hear you say! ‘We’ve heard it before’, some murmur. The European payments industry is abound with a pessimistic sense that this is already set to fail. And fail it might. But before we write it off, let’s explore some of the fundamental reasons why we believe EPI could actually be beneficial for the European payments industry.

What is EPI and what is it seeking to achieve?

The EPI is assessing potential ways of creating a pan-European payment solution

addressing the largest use cases for consumers and merchants. This builds on the traditional interbank payments space, where Europe is well standardised via SEPA and the pan-European instant payments system, SCTInst. EPI seeks to take this level of standardisation a step further – towards the consumer.

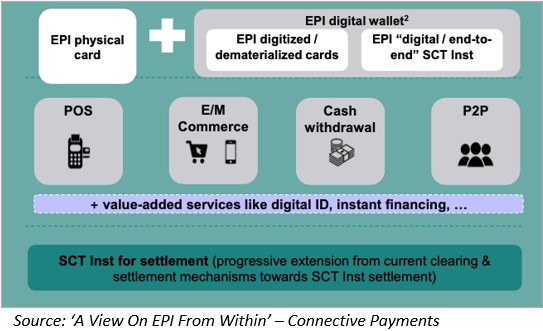

EPI’s long-term aim is to become a new standard means of payment for all transaction types. This includes in-store, online, cash withdrawal and P2P, in addition to existing international payment scheme solutions.

The initial ecosystem is being drawn up by an interim company with the aim of registering the target company in the last quarter of 2021. Although public information is limited, the EPI is initially focused largely on existing payment types (e.g. cards and wallets), and has few ambitions with regard to major, innovative improvements for European consumers and merchants.

What are the timelines?

The aim is to test a ‘proof of concept’ in 2021 before launching in the first half of 2022. There will be a three-to-four-year migration phase to EPI products and services, although it is unclear what will actually be launched in the first phase. Founding members of the EPI view the programme as a long-term investment that will deliver considerable benefits over time, rather than significant revenue streams in the first year. Indeed, at a recent ESBG webinar, Martine Weimart, acting CEO of EPI, reiterated that the programme is ‘not a short-term play but a longer-term strategy for payments in Europe’.

What makes EPI different?

The main difference between EPI and previous aborted attempts such as Monnet is that, for several reasons, political and industry support is far greater this time around.

The European Commission’s EV-P Valdis Dombrovskis has urged banks from other countries, as well as European fintechs and other European payment service providers, to join the first 16 members. That call has been heeded to a degree, with additional Spanish, Polish and Finnish banks signing up (with the Polish banks being the first to join from outside the Eurozone). In addition, equensWorldline and Nets, both European payments processors, have joined the Interim EPI Company as shareholders.

In summary, never before has a pan-European project of this nature had so much capital and support.

Why EPI could be worth it?

EPI is undoubtedly a significant undertaking, but there are two key drivers that promise to deliver significant benefits:

Finding geopolitical balance

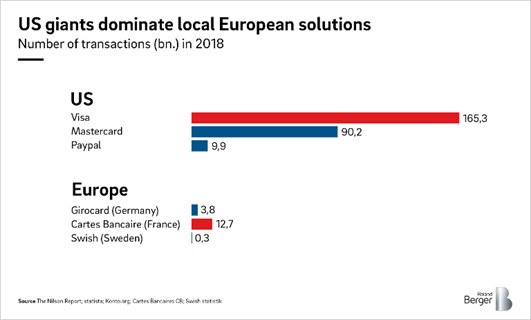

From a geopolitical standpoint, EPI makes sense. Currently, the major cross-border retail payments infrastructures that are utilised by European consumers are US-owned. From a customer perspective you could argue that this doesn’t really matter. But dig a little deeper and US hegemony across payments infrastructure and technology essentially dictates who Europe can do business with. Any regulator would take issue with that. In addition, Europeans’ share of wallet is gradually being captured by global players.

Payments also provide a crucial touchpoint for banks and their customers. Banks’ interaction with their customers is gradually eroding due to PSD2 and new players entering the payments ecosystem. EPI could be viewed as an attempt by the European banks to claw back some ownership.

Realising pan-European harmonisation and scale

Despite the major efforts from the industry in realising SEPA, the European payments market is still hugely fragmented. You can pay with Vipps in Norway, but only if you have a Norwegian bank account. You can pay with Lydia, but only in France. The list goes on and on.

While brands are important for customer trust, they play havoc with the pan-European payments experience. The reason for the great dominance of cards reflects the focus of European payment innovation that has historically been strongly tilted towards national solutions, or towards solutions covering certain regions such as the Nordics or Benelux.

But in today’s globalised world, these solutions have too few economies of scale to compete successfully with the US networks and keep up with market innovations. Martina Weimart went on to say at the ESBG webinar that ‘there is no efficiency or synergy in fragmentation’. In the long-term, investing in local solutions on a yearly basis for maintenance, security patches and other necessary updates makes large-scale innovation very difficult.

And as Europe is still a very cash-heavy economy, there is also an opportunity to convert a large portion of these cash transactions to EPI to realise a good degree of scale.

Key questions that EPI must answer

Despite the promise of EPI, there are still many unanswered questions that EPI must answer as it starts to implement the technical infrastructure:

-

What is the Target Operating Model?

The European payments industry is still in the process of delivering Open Banking and PSD2. It has also seen unprecedented adoption of digital payments due to COVID-19. Within this context, clarity is needed on what EPI hopes to bring to European payments in the long run, and the stepping stones and individual products that will be realised along the way.

For example, we do not yet know whether EPI will just be for card-based transactions, whether it covers physical and digital payments, or if it will enable Open Banking based payment initiation or request to pay over time.

A blueprint would be a useful industry guide so that other stakeholders can prepare and assess the viability of offering EPI functionality.

-

How will EPI meet pan-European requirements?

There are some fundamental cultural differences related to card payments that will need to be put aside for EPI to work on a pan-European level.

For example, French consumers cannot imagine making a payment without the option of a chargeback. This involves sharing confidential information such as the account number with the merchant. For the Dutch, on the other hand, it has been normal for years to conduct e-commerce transactions through iDEAL, with SEPA as the underlying infrastructure, without chargeback. These different payment trends and preferences are reflected across all European marketplaces.

EPI must therefore develop a plan to update scheme rules and operating procedures as banks from new markets come on stream, without disrupting what has been developed and while ensuring wider interoperability.

-

What are the key criteria for a go/no-go decision by the shareholders?

Until the final holding company has been created and the technical framework agreed, the shareholders still have the opportunity to turn away from the programme. More information is needed on the requirements for the shareholders to agree to proceed and the success factors for a go/no-go decision.

-

What is the industry engagement plan?

As we have seen with other large-scale projects, early industry buy-in is crucial. Whilst the founding banks may be invested in the process, their suppliers, other technology vendors and wider industry stakeholders are not. A comprehensive industry engagement plan, including how the supply-side of the market, merchants, and consumer groups can participate, would be greatly received. For example, we understand EPI is engaging with EuroCommerce as a representative body, but it is not clear whether merchants will have a seat around the design table.

-

How will EPI interoperate (or not)?

Many European banks may rely on Visa and Mastercard for some years after the launch of EPI, if not forever. However, it is not clear whether EPI intends to partner with the US card networks. Additionally, whether EPI intends to offer card usage internationally must be clarified where countries outside of Europe rely on Visa and Mastercard rails.

Furthermore, due to the political and sovereignty foundations of EPI, if EPI has its own brand identity, it will be interesting to see whether EPI plans to scale digital services within US-based wallets such as Apple Pay and Google Pay and allow digital cards to be integrated within them.

-

How does EPI plan to incentivise migration?

A payments system is only beneficial if there is a critical mass of users. If EPI is not mandated, there must be a plan to incentivise the likes of Cartes Bancaires, iDeal and other prominent, popular local networks to migrate to EPI. For EPI to work, there may need to be sacrifices that will be hard to swallow. Alternatively, the intention may be for EPI to become another layer of technical infrastructure.

-

Does digital currency feature on the EPI roadmap?

With a blank slate comes the opportunity to ensure a future-proof system. However, this presents its own challenges. EPI must consider where digital and crypto currencies feature in the future landscape of the network and start taking steps to address the impact of ‘known innovations’ such as the digital Euro. Mastercard and Paypal have recently announced the opportunity to use crypto over their networks, so EPI must have a plan to keep up.

The future of European payments: Bigger thinking required

In summary, EPI could potentially provide a bedrock for future European payments innovation. But rather than being too ambitious, it arguably does not go far enough.

Whilst there is merit in starting with payments products customers know and are aware of, from a technological and business point of view there is little value in European market players recreating an American wheel.

Payments are a business process and as such they should support the organisations that use them in innovative, value-adding ways. Europe is at the vanguard of Open Banking. PSD2 has seen that exciting new services can be offered to consumers that touch a wide array of products to their financial portfolio. By utilising newly built instant payments rails, both banks and fintechs can offer consumers a superhighway of financial products that are tailored to their unique life experiences. This is what true innovation looks like.

EPI should aim for loftier heights rather than merely creating a European card network or wallet proposition. A comprehensive industry engagement plan, including how the supply-side of the market, merchants, and consumer groups can participate, would be greatly received. This would help create a truly forward-looking platform for European payments, fit for the next 50+ years.

Michel Vaja