Catalysing Growth of Digital Payments in Cash-First Countries

The UK is due to upgrade its instant payments platform by mid-2025. The New Payments Architecture (NPA) aims to deliver multiple benefits, including ease of access and enhanced data carrying capabilities. In parallel, Europe has seen the launch of its real time payments scheme – SCTInst. Although voluntary to date, changes to the SEPA Regulation will see SCTInst become mandatory. In this article, Hussam Kamel, Payments Consultant, explores some of the differences and similarities between these two programmes.

Programme Objectives

Despite many of the overarching similarities between the NPA and SCTInst, the underlying aims and objectives of the two programmes are somewhat different.

At its heart, New Payments Architecture is a payment system modernisation program. The main drive is to modernise the UK’s existing instant payments infrastructure (and over time perhaps even the low value batch system, Bacs). Since the UK launched its Faster Payments system in 2008 it has seen significant rise in usage: Q3 of 2022 saw over one billion payments processed, a 14% increase on the same quarter in 2021. Most of the UK’s retail person-to-person payments now use this channel.

Since 2008, however, the market dynamics have changed significantly, and payment volumes are increasing. Critical payments infrastructure must be ready to withstand these changes, making innovation, flexibility, security and resilience more crucial than ever. As the market for digital payments grows, the infrastructure that supports it must evolve as well. This means:

- Modernising existing infrastructure

- Increase data carrying capabilities

- Ease of access to infrastructure, including API access

- Lower cost of processing payments

- Enabling effective competition and lowering the barriers to entry for new participants.

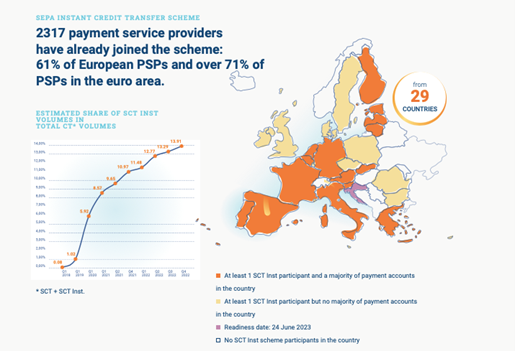

For Europe, the journey toward instant payments has been much slower. Both EBA Clearing [RT1] and STET [IP System] launched their instant payments systems in 2017, after publication of the European Payments Council SEPA Instant Credit Transfer (SCTInst) rulebook. In 2018, the European Central Bank launched its TIPS platform, allowing banks to directly settle retail instant payments in central bank money.

Fig 1: www.europeanpaymentscouncil.eu

Despite a multiplicity of Clearing and Settlement Mechanisms (CSMs), the scheme remained voluntary and, despite 71% of European banks adhering to the scheme, actual usage has been low. The European Commission Impact Assessment Report noted that by the end of 2021, only 11% of euro credit transfers sent in the EU were real time payments. This is in large part due to banks charging customers fees in line with instant payments as a premium product – some banks charge over €10 for one transaction.

The European Commission has now taken the step to mandate real time payments across the Eurozone. A key driver for real time payments is innovation for new point of interaction (PoI) solutions that would contribute to consumer choice in terms of payment method. The Commission’s vision is that an EU instant payment cross border solution would make the EU more efficient and autonomous, complementing the existing card schemes and resulting in:

- A move to a mandatory real time payments environment

- Enhanced innovation and choice at PoI

- Lower cost to consumer

- Introduction of Confirmation of Payee, to ensure trust

Governance

From a policy perspective, the NPA has been driven by the Payment System Regulator (PSR) and originated by the industry-led Payments Strategy Forum (PSF). However, Pay.UK is the responsible entity for developing the rules, standards, and vendor procurement process as well as running the system during testing, go-live, and daily operation.

In Europe, the European Payments Council maintains the underlying rulebook for the SCTInst scheme, much like it does for SEPA Credit Transfers and Direct Debits. The operating and processing of payments, in adherence with the scheme, is maintained by each of the CSMs – primarily EBA Clearing, STET, and the European Central Bank.

Standards

One of the main drivers for NPA is the migration to ISO 20022 from the existing ISO 8583-based Faster Payments. This will allow for greater data carrying capabilities and heightened opportunity for commercial data propositions. Since Faster Payments launch in 2008, ISO 20022 has become the de facto standard for payments across the globe.

The SEPA Regulation in Europe has mandated the use of ISO 20022 since 2008. All credit transfers must be conducted using ISO 20022 and in compliance with the SEPA Rulebook, maintained by the EPC.

Value Added Services

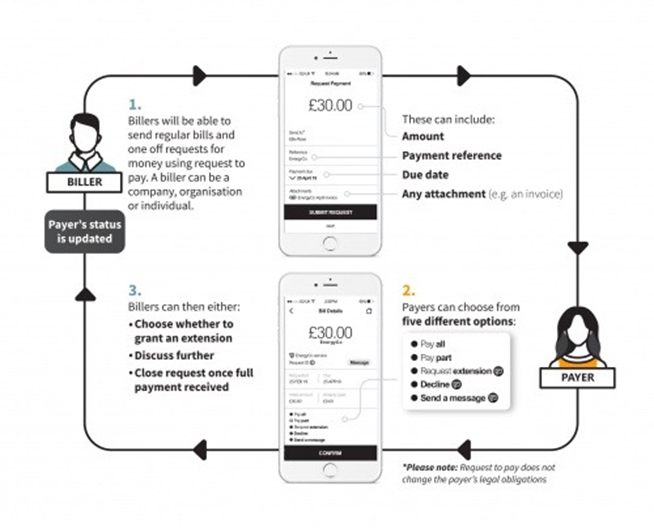

NPA will operate using a layered architecture, meaning that value-added services will be built on top of the underlying payment system. This allows different access, usage, and cost models to be implemented separate to the infrastructure. This further allows the infrastructure itself to remain lean and flexible. The UK has already implemented Confirmation of Payee (CoP), aimed at reducing fraud, as well as Request to Pay which enhances biller choice.

Fig 2: https://www.wearepay.uk/what-we-do/overlay-services/request-to-pay/

In Europe, value added service delivery is largely determined by the CSMs and the requirements of their participants. In 2021 the EPC published a rulebook for SEPA Request to Pay (SRTP). EBA Clearing launched a pan-European request to pay infrastructure service with the support of 27 PSPs from 11 European countries in 2021, based on this rulebook. In SRTP the payer-payee interaction is decoupled from the payment itself, which could mean a greater variety of service providers, including fintechs.

Under the upcoming revision to the SEPA Regulation, CoP will also become mandatory. It is yet unclear how this will be implemented across Europe. Many countries already have existing CoP solutions for their domestic markets, but it remains to be seen how cross-border CoP will be implemented. It is likely EPC will pay a role here.

Implementation Challenges

Some banks may not have the IT capacity to address the sweeping changes brought about by NPA.

- It is likely there will be a coexistence period between FPS and NPA. Banks will need to manage that coexistence and transition accordingly

- Banks serve their corporate and retail customers across many different channels – branch, web, and mobile. Consideration needs to be given to how these channels will be affected

- NPA presents large-scale monetisation opportunities, well beyond FPS. Banks must consider how to commercialise this upgrade against a backdrop of extensive industry migration projects e.g. UK RTGS renewal, T2-T2S consolidation and SWIFT.

A holistic approach to implementation must be taken to ensure the benefits are reaped and the programme does not just become an expensive compliance exercise.

The challenges of migrating to instant payments are well documented and in Europe there may still be barriers in the rollout of instant payments services to customers – both corporate and retail.

Whilst all Payment Service Providers (PSPs) carrying out credit transfers in euros will be obligated to send and receive instant payments, it is not mandatory to actively offer this service to customers. Therefore, we may still see resistance from some PSPs to promote their usage. In addition, the multiplicity of CSMs and lack of interoperability between them may lead to significant issues when processing cross border instant payments where the sending and receiving bank are connected to different infrastructures.

Timelines

In April 2023, the NPA certification testing window will open for all interested financial institutions, so existing participants in the Faster Payments scheme must be ready to begin testing for NPA during 2023. Whilst there is no definite deadline for the whole project, which is a complex, multi-year programme, it is expected transitioning all parties from Faster Payments to the NPA is expected to start around mid-2024 and will continue into 2025.

The proposed Regulation on Instant Payments was open for a feedback period of 8 weeks which ended on 5 January 2023. Feedback will be summarised by the European Commission and presented to the European Parliament and Council, with the aim of feeding into the EU legislative debate. The exact timeline of publication into the EU Official Journal – which then starts the implementation clock—is still unclear. However, the requirements will take effect in four stages:

- “[R]eceiving of IPs in euro for PSPs in the euro area: 6 months after entry into force of the Regulation;

- sending of IPs in euro for PSPs in the euro area: 12 months after entry into force; –

- receiving of IPs in euro for PSPs outside the euro area: 30 months after entry into force;

- sending of IPs in euro for PSPs outside the Euro area: 36 months after entry into force”.

How To Prepare

Despite their differences, both programmes have an important point in common: The need for banks and payment service providers to prepare and navigate both infrastructure deployment, as well as delivery of new best-of-breed products.

Institutions must develop detailed design and target architecture work. They also need to understand how they can capitalise on these changes and monetise enhanced data, real time payments and open banking initiative holistically.

Introducing both NPA and SCTInst will have a widespread and transformational impact on a bank’s existing technology estate. Banks must maintain or accelerate their own internal programmes to be ready for ‘go-live’. It is vital that the technology state architecture and delivery plan takes all details and consideration into account. Don’t get left behind.

Icon Solutions is ideally positioned to work with banks to ensure readiness for the UK’s NPA programme, and to design and build enhanced real-time-payments capabilities for banks.

For more information about preparing for the NPA programme, book a call with us today.

Arjeh van Oijen