Pan European instant payments: dream or reality?

It has been two years since the European Payments Council published the SEPA Instant Credit Transfer (SCT Inst) scheme and EBA Clearing launched RT1 – their infrastructure solution for the processing SCT Inst, bringing that scheme to life. This, combined with the TARGET Instant Payment Settlement (TIPS) system launched by the European Central Bank in November 2018, has provided a comprehensive infrastructure environment for banks to offer their customers fund transfers which are settled within seconds, all year round and all across Europe.

Two years on, how has the landscape progressed?

Are we on track for critical mass in 2020?

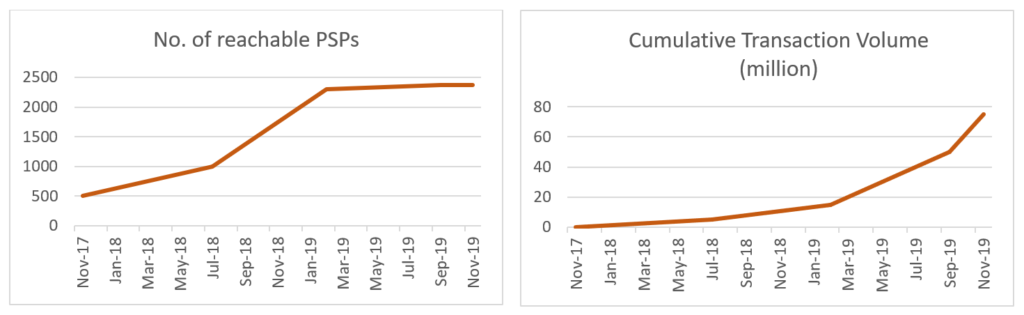

The first year of adoption saw 17 banks from 8 countries go live with the scheme extending SCT Inst reach to over 500 PSPs across SEPA. As we approach the end of Year Two numbers are currently sitting at just over 2,360 reachable PSPs (as of November 2019), located in 19 out of 36 SEPA countries, with volumes currently sitting at 3 million per week over RT1. The RT1 platform, in the two years since launch, has processed 75 million transactions.

Geographical coverage looks healthy – availability of the service in 19 countries out of 36 in the second year of launch by anyone standards is positive. Transaction volumes are steadily increasing, as is reach. Whilst not a direct comparison, Faster Payments in the UK processed over 180 million transactions in its first year, and Spanish instant payments system, IberPay processed over 20 million in its first year; putting RT1 in an average range.

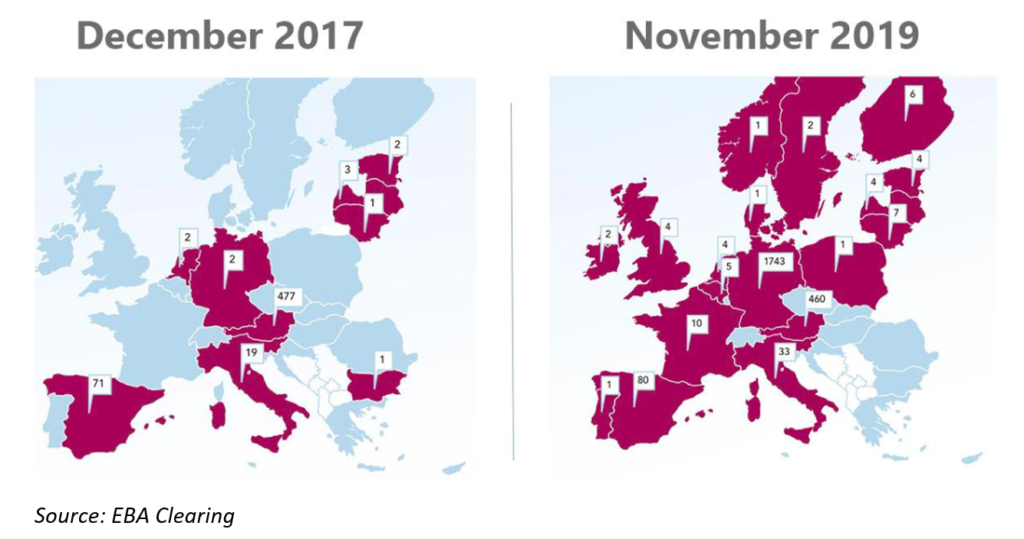

That being said, one concerning aspect is the statistics from Germany and Austria. German ‘Sparkassen’ or savings banks make up a large proportion of the reachable PSPs, as do the Austrian ‘Raiffeisenbanken’ or co-operative banks. Over 1,700 PSPs in Germany are reachable via only seven service participants. This model greatly expands the reach within Germany and Austria, nations that have not built domestic real time payments systems and are using RT1 for local transactions. However, this factor somewhat distorts the true figures when looked at across Europe.

The figures also do not tell you which banks are currently only receiving instant payments, and not offering their customers the ability to send instant payments as yet.

Payments ultimately is a network business. The value of new technology and services to users of that network will only increase as its usage does. When the number of users reaches critical mass, not being able to use that particular technology or service becomes a hindrance and gets in the way of daily life. Whilst the region is making good progress, arguably we are not there yet for cross-border instant payments in Europe.

What will spur on adoption?

Corporate usage

As stressed by the ECB, ‘the mere existence of a socially superior technology is not a sufficient condition for its implementation’ (Giannini, 2011). Individuals in today’s society most definitely want access to their funds around the clock and with immediacy, but are the real use cases for cross border instant payments – the ones that will significantly drive volume – retail based?

The scheme allows the electronic transfer of money up to the value of 15,000 euros.

In September 2019 this limit was increased to 100,000 euros, to come into effect in July 2020. This is in line with global market practice where once the system has proved itself to be safe, secure and usable, limits gradually increase over time e.g. in the UK. In Europe, this is effectively mirroring what is happening bilaterally. Deutsche Bank is allowing certain corporate customers to transfer up to 1 million euros, as are other corporate banks. This will likely promote adoption and interest amongst the corporate community.

Enhanced Customer Proposition

Whilst account-to-account instant payment transfers cross-border is attractive to a segment of the European population, embedding this offering within a wider payments ecosystem will make the proposition that much more attractive.

EBA Clearing is currently implementing a Request to Pay (R2P) solution over the top of the RT1 platform. R2P is seen as the ‘missing piece of the puzzle’ for market players to create innovative payment products and services for their customers that are based on real-time messaging as well as the SEPA schemes.

Additionally, further advancements in payment initiation at Point of Sale will greatly advance instant payments adoption imbed them into daily life. Twenty European banks are reportedly working on the development of a rival payment system to challenge the dominance of Visa and Mastercard as well as Chinese and US Big Tech firms. The Pan European Payment System Initiative (Pepsi) would handle all forms of cashless transactions. Furthermore, QR codes at Point of Sale will spur on adoption. The EPC launched a standardised QR code for European payments. Already heavily used in countries like Sweden, Switzerland has also launched a Swiss QR code for retail and corporate customers. This can assist in real time bill payment as well as in the retail sector.

The industry has also yet to see the real impact of PSD2 Payment Initiation Service Providers in the market. As attention shifts from account aggregation services towards payment initiation we will likely see an upsurge in the usage of instant payments.

Flexible Access Models

There is no doubt that with SCT Inst being an optional scheme, smaller banks have struggled to justify the expense. They have had their wallets effectively sewn shut thanks to GDPR and PSD2. As payments and payments innovation becomes more heavily regulated, optional services must compete for budget against mandated initiatives that require heavy investment. Instant payments may just fall into the long list of ‘nice-to-haves’ but not essentials for lower tier banks. Therefore, alternative access models are vital for reachability in the absence of a mandate. RT1 and TIPS are both looking at access and pricing models, which will hopefully result in greater optionality for smaller banks. The implementation of ECB’S TIPS has given a low-cost option. TIPS operates on a full cost-recovery and not-for-profit basis. There are no entry or account maintenance fees. The price per instant payment transaction is fixed at 0.20 eurocent (€0.002) until at least November 2020 and the first 10 million payments made by each TIPS participant before the end of 2019 are free of charge. There is a real push from the ECB to encourage a range of market players to participate. With 28 participants and 1114 reachable PSP’s, numbers are growing.

Interoperability

Perhaps one of the most important success factors is the interoperability of instant payments infrastructures. Competition and optionality in the infrastructure is essentially now a part of the European landscape due to the launch of RT1 and TIPS. The ECB has stated the goal that a bank should be able to connect to only one Automated Clearing House (ACH) to achieve pan-European reach for instant payments. In order to attain this goal, the ACHs need to be interoperable. Achieving interoperability between ACHs is not an easy task, as each has its own infrastructure and system rules. EACHA recognised the need for guidance and drafted the EACHA Instant Payments Interoperability Framework, which stipulates standards ACHs can adhere to when organising bilateral interoperability. It is not clear how effective this interoperability currently is within the instant payments ecosystem.

Instant Payments strategy

Lastly, banks need a cohesive strategy around instant payments and value-added services. This should include a solid view on how to migrate payments volume across to instant payments to promote low cost usage. This needs to take a holistic view of not only instant payments as a transaction type, but also real time data analytics, data use cases and monetisation. Instant payments needs to be a supportive factor in a banks long term strategy.

Europe is on a solid trajectory of growth in the instant payments sector. More will need to be done to make the cross-border element a success. The development of value added services for both corporate and retail customers will certainly drive adoption. We are likely to see critical mass in terms of reachable PSPs by 2020 but in terms of usage, we are still a way off.

Lauren Jones