The opportunity for instant international payments

It’s been said a number of times – instant payments are the new norm, but what about international payments? Could there be the possibility for these to become instant too? In my view, this could be achievable – the path wouldn’t be easy of course, but I don’t think the idea is unfeasible.

Correspondent Banking

Let’s take a look at correspondent banking. Currently, there are limited mechanisms for making and settling international payments and very few for international instant payments. SWIFT, for example, uses a complex sequence of messages to move money between (potentially chains) of correspondent banking partners to make and fund payments.

The SWIFT payments infrastructure started as a patchwork of correspondence banks, FX markets, and central banks that have evolved over the years to facilitate cross-border value transfer. It’s reflective of history and, despite the SWIFT global payments innovation (SWIFT gpi) in 2017, connectivity to TIPS in Europe and some recent proof of concept work in Asia, doesn’t yet reflect the modern potential of current technology, which can enable real-time payments globally that settle with minimal transaction cost.

SWIFT state that, since going live in 2017, 50% of gpi payments are credited to the end-beneficiary account within 30 mins and many within seconds. Where multiple banks are involved in a payment chain, the final leg needs to be cleared within the recipient country and the domestic payments are sometimes delayed owing to the limited operating hours of the local clearing systems.

Without a global real-time settlement system some payments may take a considerable time before monies are made available to fund the eventual payment.

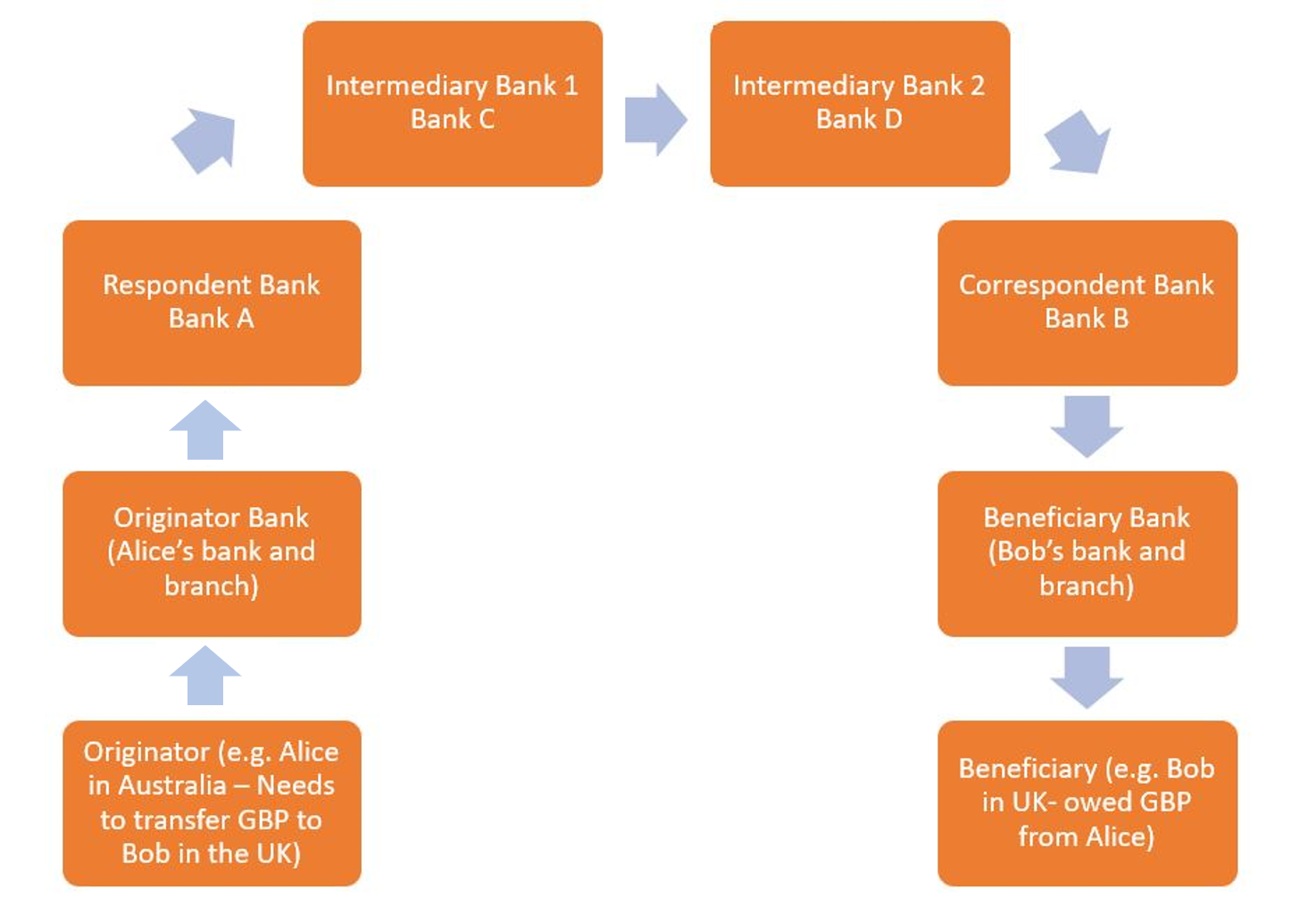

This may be acceptable for complex transfers:

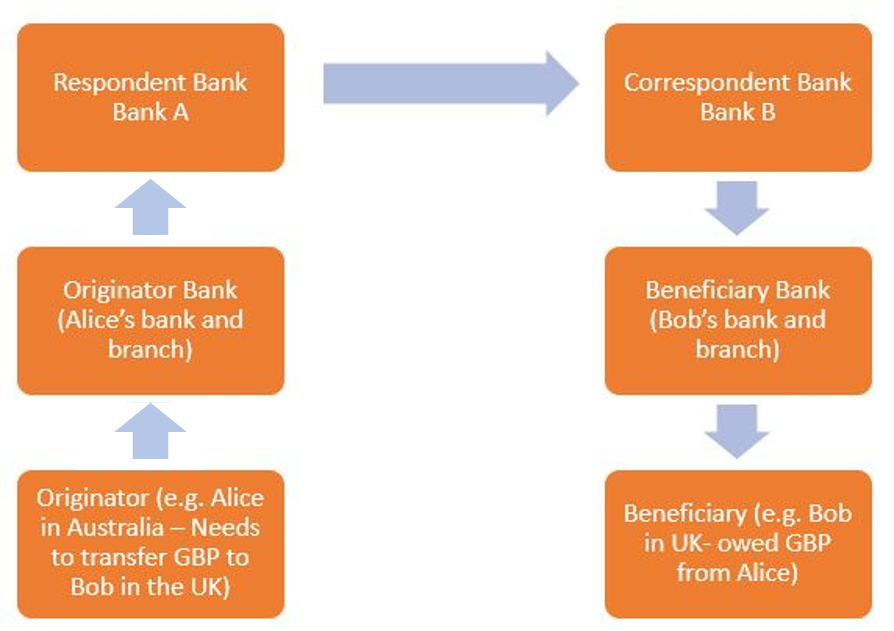

However, this seems protracted and complex for simple payments:

In the longer term, it is likely that real-time cross-currency settlement schemes and systems will eventually link the correspondent banks, which will remove the need to maintain the expensive (KYC, KYCC, etc) relationships. However, these schemes will need to address liquidity across multiple currencies together with fluctuating foreign exchange rates amongst other things, meaning this is unlikely to happen any time soon.

As an interim, some progress has been achieved with real-time settlement schemes linked by systems such as the European TARGET Instant Payment Settlement (TIPS) with the intention of providing settlement across schemes. As a proof of concept, SWIFT Instant Payments has linked several banks across Asia taking advantage of their domestic real-time payment systems to enable some immediate payments. Other countries have developed their own bespoke solutions, for example, Hong Kong have a near-real time payment versus payment settlement solution for HKD to USD, Euro or RMB using their Cross-Country Payments Matching Processor. There is evidence of progress being made; however, instant international payments that settle in real-time globally is still a future aspiration.

Given that correspondent banks already maintain liquidity to fund payments made through their correspondent partners and that many banks are implementing open banking APIs (e.g. PSD2, ‘Open Banking’), perhaps there is appetite for an interim non-scheme solution for real-time payment initiation?

Another option – using an Open Banking API

The advantage of this option is that you could leverage correspondent banking relationships (with their existing liquidity management mechanisms) and enable Open Banking functionality for a bank’s accounts held with their correspondent partners.

So, for example, instant payments could be enabled from a customer’s account held at a bank (via that bank’s nostro account held with their correspondent partner) to a beneficiary’s account held at either the correspondent bank or a bank that is connected via an instant payment scheme to the correspondent bank.

The Open Banking functionality also offers additional benefit in managing the originator bank’s liquidity (specifically, the balance held in their nostro account with their correspondent bank), through, for example, real-time balance enquiry.

Settlement uses existing mechanisms

- The balance of the originator’s account is reduced by the value of the payment, crediting this amount to the originator’s bank.

- The originating bank’s nostro account is reduced by the value of the payment crediting this amount to the beneficiary’s bank.

- The beneficiary’s bank credits the value of the payment to the beneficiary’s account.

Limitations and Constraints

- Operations on the sending bank’s nostro account can only be made by the sending bank. Other banks that are co-members of schemes that connect to the sending bank would have no authority to initiate payments from the correspondent accounts.

- Payments can only be sent to beneficiaries that have accounts held by the correspondent bank or a bank that is linked to the correspondent bank via an instant payment scheme.

- The bank offering the open banking capability against a vostro account that they are hosting, must be happy with the proposed usage, through KYC, KYCC and their risk policy.

- The bank offering the open banking capability against a vostro account will need to be prepared for the expected volume of payments flowing through that account.

- The liquidity (pre-funding) of the sending bank’s nostro account will limit the value of instant payments that can be made using this mechanism (this is unchanged from the existing limitation on SWIFT based correspondent banking payments).

- If utilised, local instant payment schemes may restrict payment maximum values.

- To leverage open banking APIs, banks need to register with the monetary authority of the beneficiary country (e.g. FIs need to register with CMA in UK).

- The Open Banking API, although based on the common ISO 20022 messaging standard, does vary between countries and the bank implementations. Therefore, banks adopting this approach would need to maintain several API standards for every country they wish to send payments to.

And of course, compliance considerations…

A bank offering Open Banking functionality to their correspondent banking partners must accept the risk. Given the limitations above, this should be a subset of existing business rather than new activity.

AML monitoring

Currently, international payments must comply with AML and other regulatory checks. Since the Open Banking API does not currently cater for the payment originator’s details (i.e. the beneficiary bank’s nostro account is not the actual originator), either the originator’s bank must be responsible for these checks (this would require regulatory guidance/agreement) or an extension to the open banking API would be required to supply the necessary details of the true originator to enable the checks.

Targeted API Usage between a Bank and its Subsidiaries

Considering the AML concerns and the potential variance in API standards across countries and banks, perhaps international banks wishing to adopt this approach could do so for their subsidiaries’ customers only (i.e. between customers who are known to the bank and already cleared in respect of AML checks). Certainly, this would address much of the compliance concerns.

A matter of time

I think it is clear that, by building on the frameworks of Correspondent Banking and Open Banking APIs, it would be possible to construct a mechanism for instant international payments but there are some key considerations that need to be overcome. In a real-time world it will only be a matter of time before consumers are demanding immediate instant payments. Banks who start to explore the possibility will be well placed to meet this future demand.

Colin Weeks